Update from the Austrian Supreme Administrative Court: prohibition on deduction of manager remuneration in connection with the research premium generally not applicable

In its recently published decision (30/09/2025, Ro 2024/13/0017-6), the Austrian Supreme Administrative Court (VwGH) ruled that the prohibition on deduction of manager remuneration pursuant to section 20 para. 1 subsec. 7 Austrian Income Tax Act (EStG) is not applicable for calculating the assessment base for the research premium, thus amending the Austrian Federal Financial Court […]

Background on Import One Stop Shop (IOSS) Basically, IOSS is a system, through which value added tax (VAT) for import distance sales within the EU can be declared and paid electronically. Subsequently, the obligation to register in the country of destination no longer necessary for suppliers from third countries. Goods with a value of up […]

Country-by-Country Reporting (CbCR) serves to provide information that enables tax authorities to conduct an informed risk assessment of transfer pricing. In May 2025, the OECD published a new overview of common errors made in preparing CbC reports. The document updated the summary from November 2019 with further common errors, reaching a total of 28. As […]

Failed triangular transactions – VwGH submitted questions to the ECJ again

With resolution dated 7 October 2025, the Austrian Supreme Administrative Court (VwGH) submitted key interpretative questions regarding the simplification rule for triangular transactions to the ECJ. The focus is on whether an invoice correction related to failed triangular transactions is possible and whether the invoice correction has ex nunc effect. VwGH 7 October 2025, Ro […]

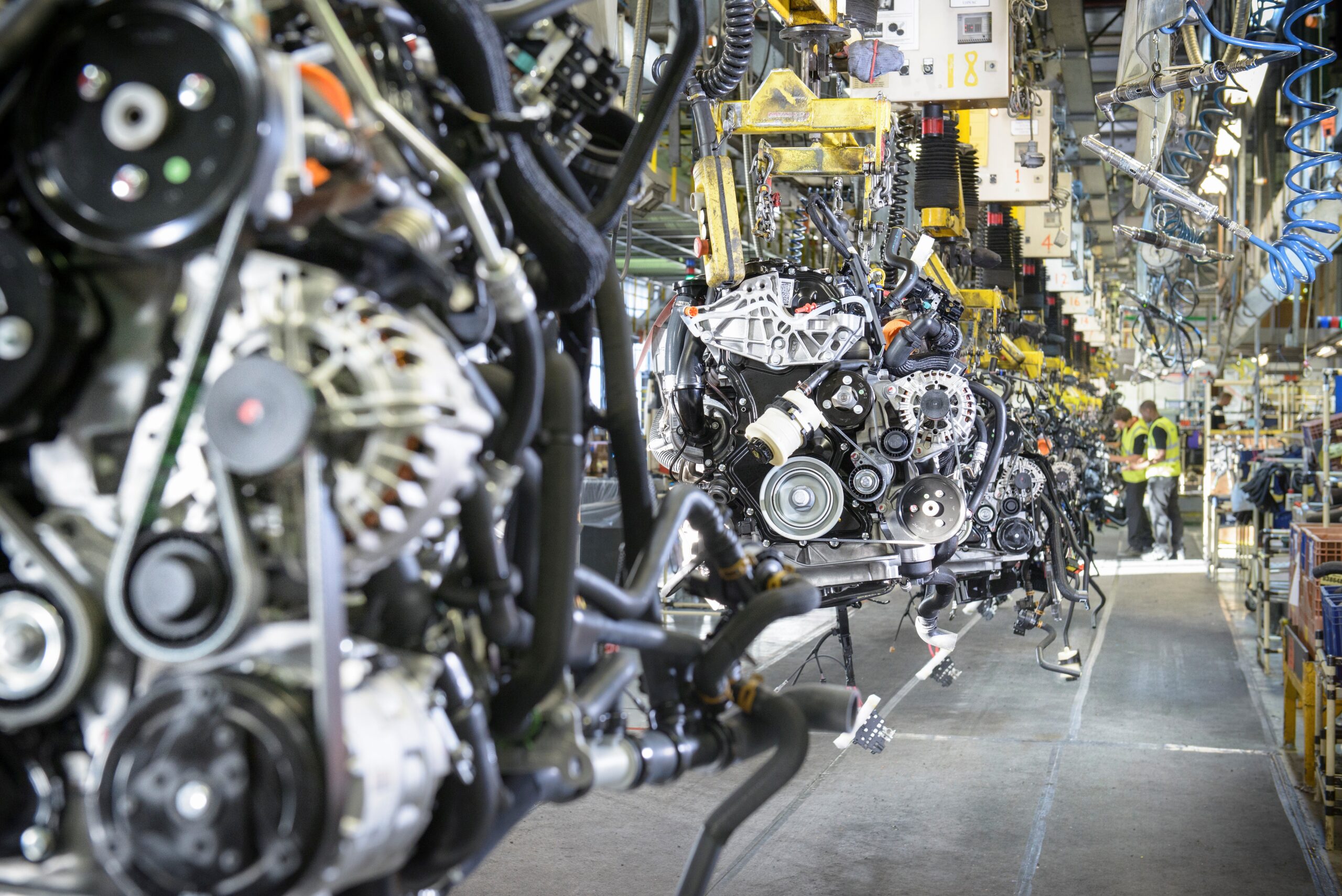

ECJ on VAT treatment of supplies of equipment and dies

On 23 October 2025, the ECJ has commented on the VAT treatment of supplies of tooling equipment with reference to the legal case Brose Prievidza C‑234/24. Underlying case The German automotive component manufacturer Brose Coburg acquired specific tooling equipment from the Bulgarian supplier IME Bulgaria for the manufacture of components and sold it to the […]

Austrian Supreme Administrative Court (VwGH) confirms: receivables bearing no interest qualify as capital assets within the meaning of section 27 Austrian Income Tax Act (EStG)

Recently, the VwGH (4/9/2025, Ro 2023/13/0010) confirmed that the capital appreciation tax introduced with the Austrian Budget Accompanying Act 2011 (BBG 2011) “product-neutrally” includes all assets generating income in principle subject to section 27 para. 2 EStG in non-business contexts. Whether the respective asset actually generates income from the provision of capital assets or qualifies […]

Council decision – important updates to the Carbon Border Adjustment Mechanism (CBAM) from 2026!

On 29 September 2025, the Council of the EU signed off on simplifications to the CBAM Regulation through the Omnibus package. The amendments seek to provide simplification and cost-efficient compliance improvements to the CBAM, taking effect from 1 January 2026. Please find the most important updates below: Setting a single mass-based threshold (de minimis rule) […]

Two-factor authentication (2FA) Previously, FinanzOnline login worked either using ID Austria or a user name and password. From 1 October 2025, login using two-factor authentication (2FA) will be mandatory for all those who have previously only logged in with a user name and password. Therefore, these changes affect all those who do not use ID […]

DAC7 – implemented in Austria by the Austrian Digital Platform Reporting Requirement Act (DPMG) – continues to pose major challenges for platform operators. After the second year of the DAC7 reporting obligation, there are still many uncertainties regarding the report, not least how to proceed if corrections are required after submitting the report. The German […]

ECJ on VAT treatment of transfer pricing adjustments

With its decision in the case SC Arcomet Towercranes(C-726/23) published on 4 September 2025, the ECJ takes a stance on VAT effects of transfer pricing adjustments (“TP adjustments”) for the first time. Description The SC Arcomet Towercranes SRL (subsidiary) is part of the Arcomet group. The Romanian subsidiary buys or rents cranes for selling or […]

Wir verwenden auf unserer Website Cookies, um die Nutzung bestimmter Funktionen der Website zu ermöglichen, für die Webanalyse, um das PwC Serviceangebot kontinuierlich zu verbessern und Ihnen ein besseres Nutzererlebnis zu bieten. Diese Einwilligung kann jederzeit über Ihre Browser-Einstellungen mit Wirkung für die Zukunft widerrufen werden.

Diese Webseite benutzt Cookies zur Verbesserung Ihrer Nutzererfahrung und unseres Informationsangebotes. Wir verwenden verschiedene Cookie-Arten: Essenzielle Cookies zur Erreichung der Funktionen der Webseite (zB. Spracheinstellungen). Weiters nutzen wir Cookies von Drittanbietern um zu verstehen, wie Sie unsere Seite nutzen. Diese Cookies sind nicht notwendig für die Funktionalität der Seite und Sie können daher der Setzung des Selbigen widersprechen.